.avif)

If you follow innovation in mortgage tech, you’ve probably heard the buzz around Direct Mortgage Corp., a U.S. mortgage banking company that serves borrowers across multiple loan types nationwide. They recently reported an 80% return on investment (ROI) after transforming how their loan files move through underwriting and closing.

That number turns heads—but what’s behind it?

Their success wasn’t about a new LOS or another OCR plugin. It came from deploying agentic AI — intelligent systems that don’t just automate individual tasks but coordinate the entire lending workflow.

Direct Mortgage Corp.’s ROI didn’t come out of thin air. It’s tied to measurable, mechanical improvements — faster cycle times, fewer manual touches, and lower defect rates.

If you look at public benchmarks from Fannie Mae’s Day 1 Certainty® program, those efficiencies make sense. Fannie has long documented cycle-time reductions of 6–20 days when multiple digital validation features are used. By verifying income and assets directly from source data and relieving certain reps and warrants, lenders clear loans faster and more reliably.

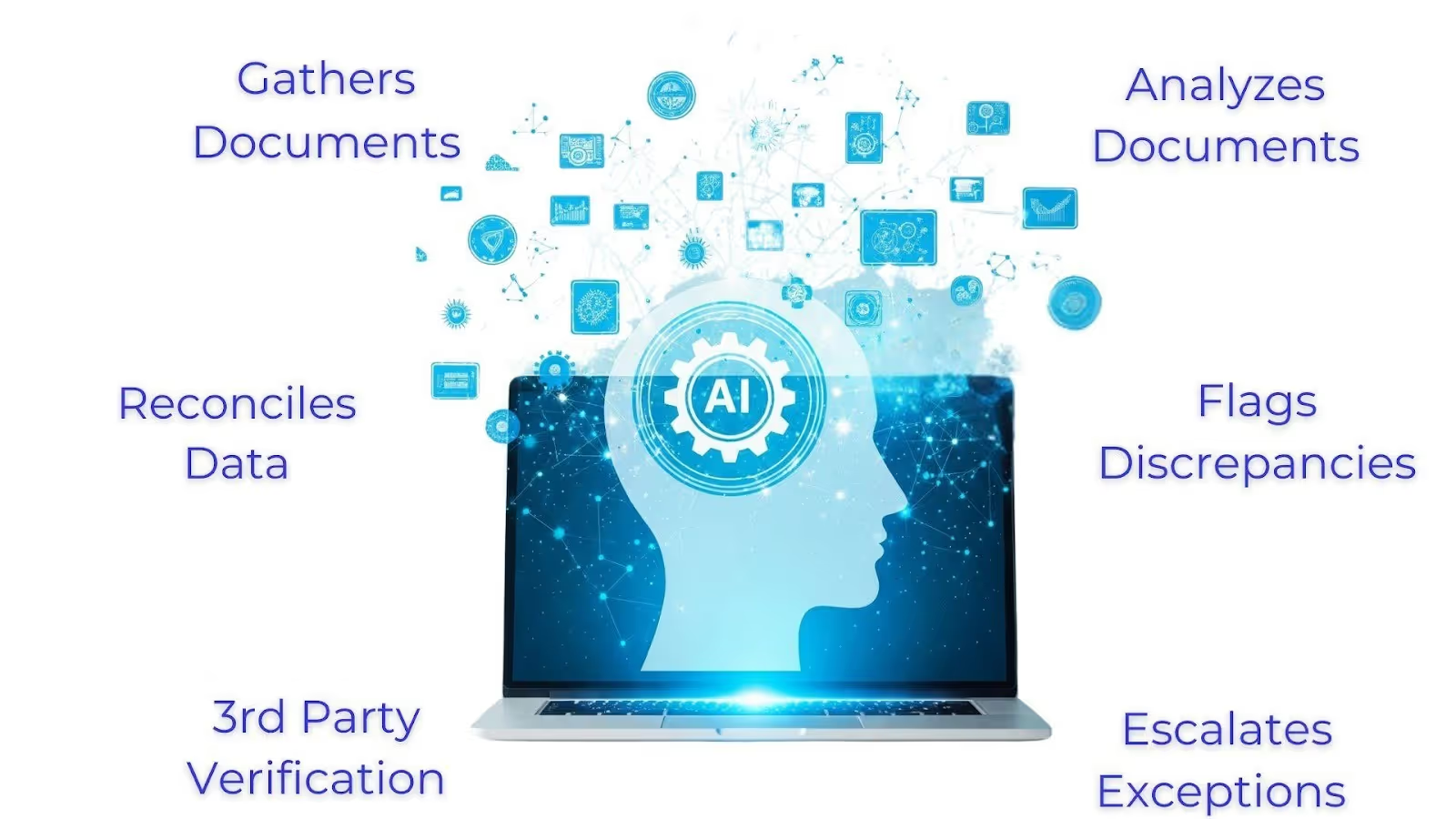

Now imagine going beyond just data validation. Agentic AI takes that concept further—automating and orchestrating the full workflow rather than just one step.

Traditional automation in mortgage focuses on OCR, data extraction, and rule checks. Useful, but limited.

Agentic AI, by contrast, acts more like a digital team:

This isn’t science fiction — it’s how forward-thinking lenders like Direct Mortgage are already working. Research from McKinsey and Bloomberg points to the same conclusion: AI agents will reshape banking and mortgage lending by automating complex, multi-step processes from end to end, not just speeding up one task.

Let’s break down the main drivers behind that return.

1. Cycle-time compression.

Faster time-to-clear means higher throughput and lower per-file costs. According to agency data, digital verifications can already shave days off closings. When AI agents run those workflows, some lenders are seeing 60–80% cost savings compared with manual verification paths.

2. Defect and rework reduction.

Agent-driven exception handling prevents expensive post-closing cures by catching issues early.

3. Labor leverage.

AI handles document collection and checklist management, so underwriters and processors can handle more files per FTE.

4. Risk management.

Predictive scoring and triage from agentic systems lower fallout and early-payment default exposure. Studies show delinquency rates dropping as banks adopt AI-based risk models.

Put together, these effects easily justify an ROI in the range that Direct Mortgage Corp. reported.

By 2026, competitive pressure will be intense. Large lenders are already “rewiring” around intelligent workflows.

McKinsey’s banking analysis warns that institutions that fail to adopt AI agents risk margin erosion. Meanwhile, PwC’s Responsible AI survey shows enterprise adoption accelerating—with benefits in transparency, risk control, and customer experience.

For SME lenders, agentic AI isn’t optional—it’s the practical path to staying cost-competitive while keeping turn times, compliance, and borrower expectations in balance.

Generic chatbots and OCR services have their place, but they don’t understand your overlays, investor rules, or SLA commitments. The real gains happen when your policies, exceptions, and loan-program rules are encoded directly into the AI agent’s decision policy—and when that agent has the authority (and integrations) to move a file forward.

As McKinsey puts it, the winners will be those who build workflow-aware, custom AI agents, not those who bolt generative AI onto legacy systems.

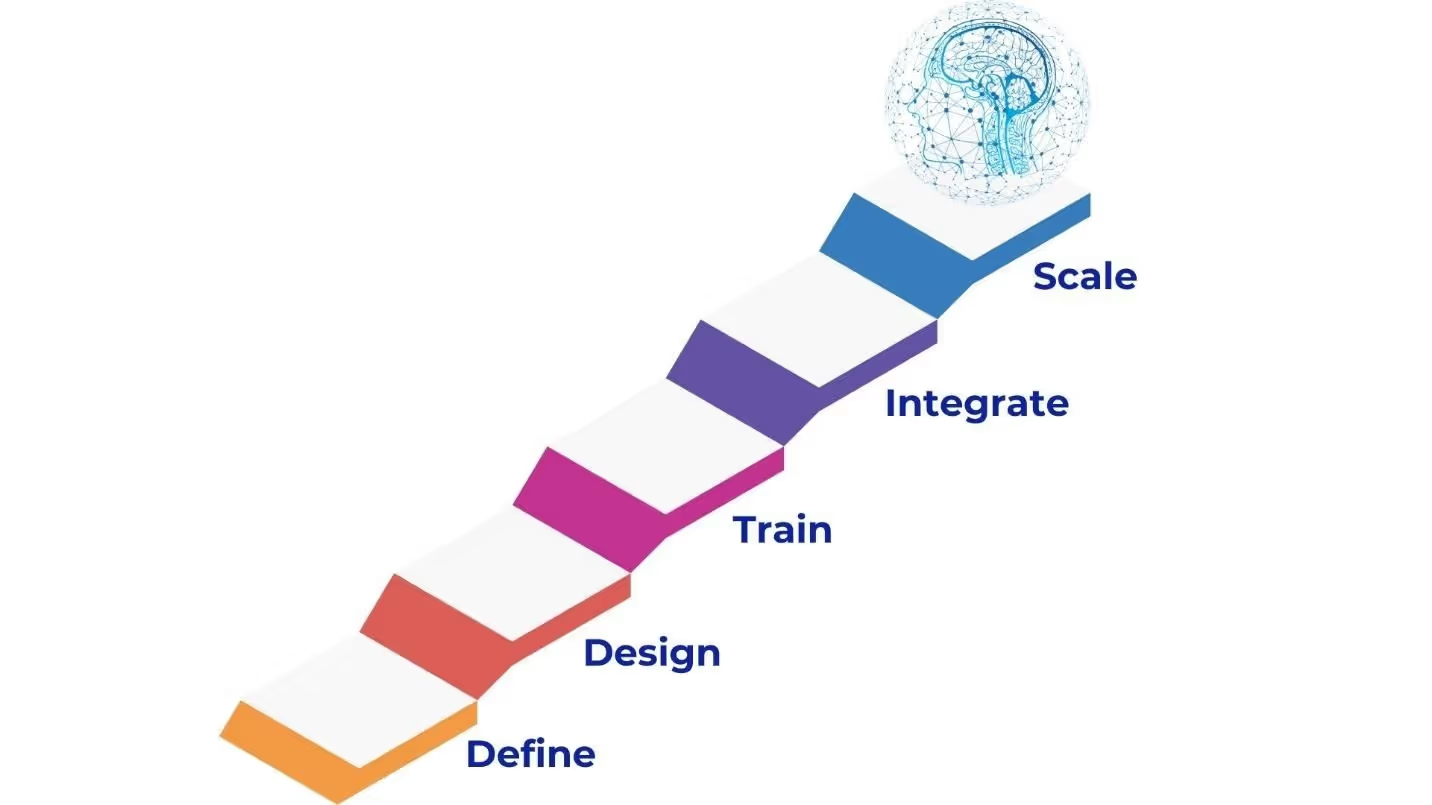

Here’s how smaller lenders can follow Direct Mortgage Corp.’s lead:

Direct Mortgage Corp.’s 80% ROI is proof that when a lender moves from task-level automation to agentic orchestration, the economics shift dramatically.

By 2026, SME lenders that deploy custom AI agents aligned with their own policies and workflows will fund loans faster, at lower cost, and with fewer defects. Off-the-shelf tools may help at the margins—but custom agentic systems deliver structural advantage.